Changing Fortunes: Tracking 20 Years of Returns Across Credit and Venture Capital

Changing Fortunes: Tracking 20 Years of Returns Across Credit and Venture Capital

Last month, the Federal Reserve announced its first cut to interest rates in over four years. This is expected to be followed by more cuts into early next year, reversing the trend of increasing rates throughout the 2020s.

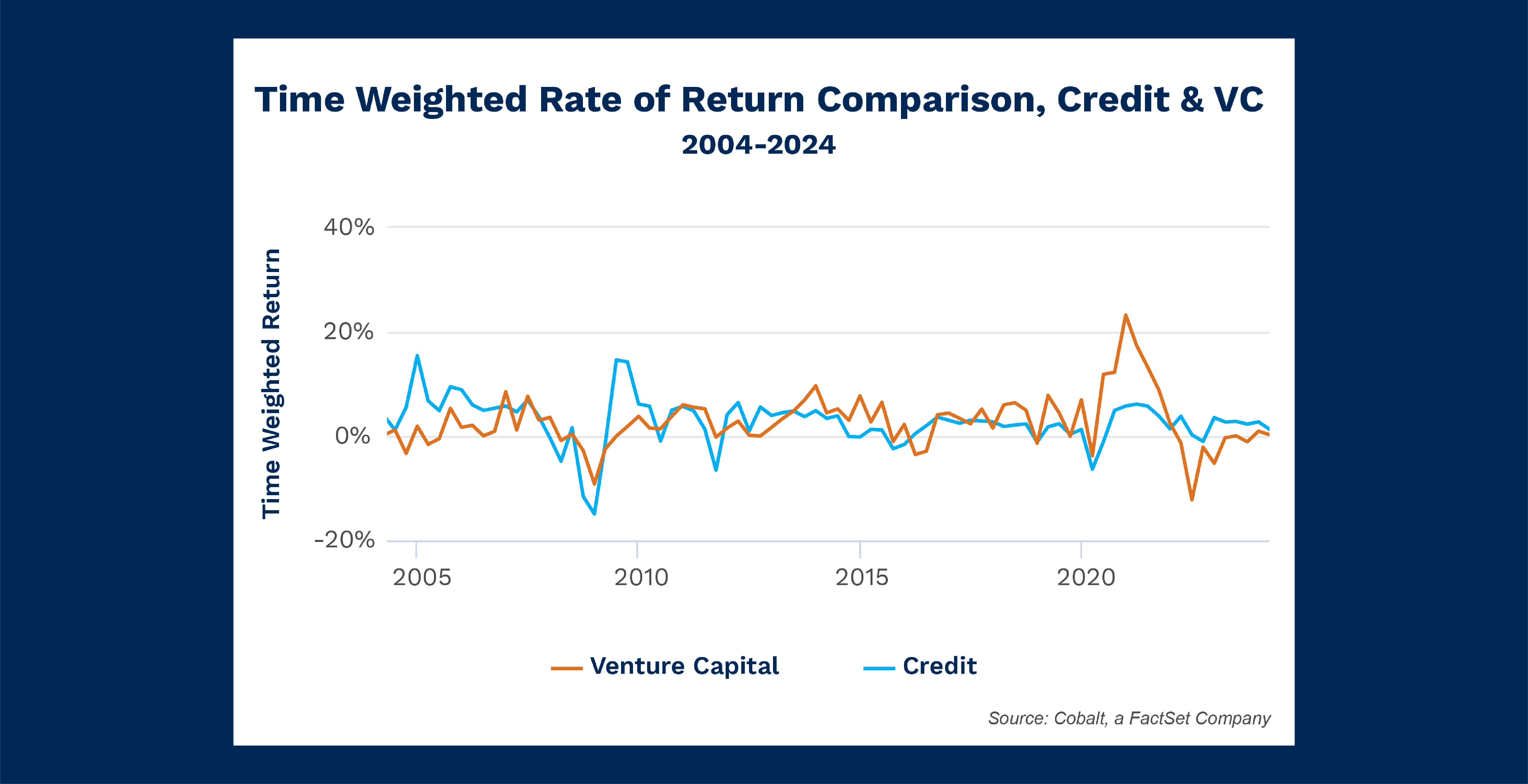

With this in mind, we analyzed the returns of credit investments in our dataset and noted how it tracks through different policy adjustments and environments. For the analysis, we pulled the Credit Time Weighted Rate of Return (TWRR) and included the same metric for venture capital. VC offers a good counterpoint to credit, as they have different risk profiles that would be expected to behave different under various macro stressors such as inflation and high-growth environments, for example.

Key Takeaways

As anticipated, VC and credit offer many different quarters and periods of divergence over the past 20 years. This is a helpful pairing to highlight how different environments effect credit.

Conversely, credit much more closely follows a strategy like buyouts. In fact, over the 20-year sample period, credit and buyout returns were within 1% of each other for 23 quarters, or 28% of the time. This level of similarity created a pattern where the dips and recoveries very closely mirrored themselves across different macro environments.

The last two recessions best illustrate how the macro climate can shape performance among these strategies in different ways. Coming out of the global financial crisis, credit experienced four quarters of outsized returns, benefiting from undervalued distressed assets. Meanwhile, venture rebounded as well, but more mildly, as the recovery from the crisis was less conducive to startups and tech.

The roles were reversed at the start of the 2020s, as VC experienced sharp recovery from the COVID bottom-out. Fueled by cheap money in a low-rate environment, VC had seven quarters of market-beating returns, but has been mired in two years of underperformance as inflation and a tightening economy took control.

Conversely, credit didn’t experience the peak performance through the end of 2020, but it has steadily produced returns in recovery and outperformed VC since Q1 2022, with a more beneficial high-rate environment and less of an impact from large-scale events like the bank failures of 2023.

Looking Ahead

Outside of a roughly five-year window at the end of the 2000s, credit has been the more consistent strategy quarter-over-quarter dating back to 1995 when our dataset starts. With this track record, we expect that trend to continue holding through the rest of the 2020s.

This may hold true even as rates are cut, which historically has been a boon for VC returns. If this leads to outsized returns a few quarters down the road for the strategy, we still expect the quarterly consistency to remain on credit’s performance.

Subscribe to our blog:

Is There Geographic Bias in Macro Liquidity Trends in Private Markets?

Is There Geographic Bias in Macro Liquidity Trends in Private Markets? Building on our previous analysis of the role of…

Private Equity Performance: Large Strategies Versus Funds of Funds, Co-Investments, and Secondaries

Private Equity Performance: Large Strategies Versus Funds of Funds, Co-Investments, and Secondaries In private equity, the large strategies of buyouts,…

Examining Tariff Policy Impacts on Private Fund Contribution Rates

Examining Tariff Policy Impacts on Private Fund Contribution Rates Recently we examined the impact of Latin America presidential elections—which carry presumptions…